Retail CIO Outlook Weekly Brief

Be first to read the latest tech news, Industry Leader's Insights, and CIO interviews of medium and large enterprises exclusively from Retail CIO Outlook

DAVE: “Open the pod bay doors, Hal.” Stephen Barnham, SVP & CIO, MetLife Asia

Stephen Barnham, SVP & CIO, MetLife Asia

HAL: “I’m sorry, Dave. I’m afraid I can’t do that.”

This now infamous scene from Stanley Kubrik’s 1968 classic, “2001: A Space Odyssey,” where the Discovery One’s HAL 9000 computer refuses to open the pod door, is emblematic of our early perceptions of Artificial Intelligence (AI). Yet as technology has marched forward at an exponential rate, AI has shifted from science fiction to science fact.

"AI and enhanced mobile technology is changing the way we live and raising expectations for how we interact with the brands around us"

Half a century on, AI is all-pervasive – embedded in our smartphones, cars, and homes. We have digital assistants that tell us the weather forecast and order our groceries. We have come to expect an ever-greater level of personalization in how we experience and purchase products, for example the cosmetics industry is now using augmented reality to show customers what products look like on their own face.

Without a doubt, AI and enhanced mobile technology is changing the way we live and raising expectations for how we interact with the brands around us. Insurance is no exception. While the industry has traditionally been seen as slower to jump on new technology trends, the sector is quickly seeing potential in AI and machine learning to create differentiated customer experiences and improve back-end processing.

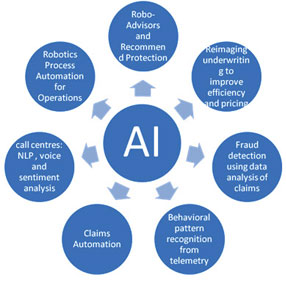

For example, we are now using trained signal processing technology to dynamically understand interactions between call centre agents and customers. The technology is able to detect and analyse emotion, sentiment, confusion, and overall level of engagement to advise and coach call centre agents to better understand and respond to customers’ needs in real time.

Underwriting presents another big opportunity. Today’s digital ecosystem represents a wealth of unstructured, fragmented, health-related information embedded in medical research, claims histories, and social media. Layered into this, you now have troves of customer opt-in data collected through sources like wearables that, if effectively aggregated, could fundamentally transform underwriting and better align the relationship between insurer and customer. The ultimate goal for insurers is to simplify and personalise the underwriting experience, using data analytics, to eliminate the need for intrusive questions and to create an experience that feels like the company intuitively ‘knows me’.

The new model would be faster, easier and more accurate. More importantly, it may expand coverage to individuals that previously couldn’t be covered, because the analytics would allow the insurer to become proactive partners in improving customer’s health, helping them manage illness and enable them to live long and heathy lives.

We are already seeing AI play an increasingly active role in the auto insurance industry. Black-boxes that track the quality of a motorist’s driving, have changed the pricing landscape and AI is now helping to improve efficiency on the back-end with one insurer using it to interpret photos of collision damage for claims loss adjustment.

AI is also offering significant efficiency benefits to insurers when it comes to back-end processing. Many insurers have large, paper laden back offices, AI driven robotics is helping to automate manual, mainly monotonous tasks to free up staff for more value added activities. Insurers are also using AI pattern recognition and big data algorithms to trawl vast troves of claims data to reduce cases fraud, which would have previously been difficult, and time consuming to detect. For example if a medical practice is consistently issuing unnecessary prescription drugs that don’t match the patient’s diagnosis, AI can be used to detect these patterns of fraudulent activity.

With so many successful examples of AI already in play, it’s no surprise the industry is doubling down on this trend. It’s also opening the door to new digital-first entrants, looking to take of their vast their datasets to provide deeper insights on morbidity and mortality to efficiently and accurately price products.

Concurrent to the explosion in AI applications across the sector, the continued expansion of cloud services has also given rise to a bourgeoning community of startups focused on insurtech (insurance technology) that are building powerful AI tools to compete in niche areas like on-demand personal property insurance that offers "micro-duration” policies, or AI facial analytics to predict life events.

Insurtechs now fill a vital role in the industry’s innovation ecosystem and like many larger industry incumbents, MetLife is determined to capture this opportunity. We have a holistic approach, bringing external orientation and internal efforts together to accelerate innovation and create tangible enterprise value. This includes strategic partnerships with leading tech companies and venture capital firms; collaborations with academic institutions like MIT; a USD $100m co-investment fund; and our Singapore-based innovation centre,“ LumenLab.”

This is an industry truly on the verge of rapid transformation. What exciting twists and turns it will take over the next decade, remains to be seen, but for an industry that is very familiar with risk, the biggest risk we ourselves now face is complacency. The message is clear: it’s time to embrace the change and reimagine our business.

Read Also